Buying a House in the US: Six Tools & Tips to Do it Right.

If you google 'How to buy a House?', you will find a hundred step-by-step guides at your disposal. Yet, almost all of them only prepared me partially for my home-buying experience. I have elucidated the process with my personal experience. They can offer practical suggestions to new homebuyers.

In the Spring of 2022, we decided to take the plunge and buy a house. We contemplated the idea for almost two years before deciding to do it. If you google 'How to buy a House?', you will find a hundred step-by-step guides at your disposal. Real estate listing websites, mortgage banks, or brokerage firms write these articles to emphasize different things and collectively provide a perspective on home buying. Yet, almost all of them only prepared me partially for my home-buying experience. I have elucidated the home-buying process with my personal experience. They can offer practical & valuable suggestions to prospective homebuyers. To the general reader, the analytical approach to solving any real-life problem using excel sheets might come in handy in dealing with other situations.

Make sure you are ready; Financially & Mentally.

Buying a house means responsibilities. It means you either spend time or money fixing things. While money can buy most things, there are a few things you still have to do. So be prepared.

Financially, it will mean putting aside a significant downpayment and adjusting to a new monthly mortgage which is more often than not higher than rent. Ensure you have an emergency fund (typically six months of household income) to deal with unexpected situations.

Buying a house beyond your means is a sure shot of the recipe for hardships. Typically, the house price should be less than three times the total household income before taxes. Put another way, the monthly expenses from the house should be less than 30% of your monthly paycheck. These numbers aren't typical for the state of California & Washington, but increasing your downpayment to keep it as suggested above would be wise.

Although we were financially ready to buy a house for almost two years, we hesitated to take the plunge until we both had jobs in the same city. More importantly, we wanted to space out all significant milestones in life. Since we just had a baby, we decided to push the timeline further down the line.

Start looking for houses. Slow burn

Go on Zillow, Redfin, or any other real estate marketplace website and look for houses that are attractive to you. Then schedule a visit using an agent from recommendations through the app or elsewhere. It helps you get a feel for the city, community, types of houses available, and the money you need to shell out. Ask around (friends, family, colleagues) to educate yourself. Never rely on a single source for any piece of information. It gives you an insight into the market and helps you form a perspective.

It also helps you narrow down on a realtor who is good at his job: willing to show you as many homes as necessary, understands what you need, makes meaningful suggestions regarding locality, price, making an offer, etc.

We looked at around 10-15 houses and worked simultaneously with multiple real estate agents. It helped us frame our wild ideas into practical solutions. It also helped us narrow down a real estate agent who was proactive in showing the houses.

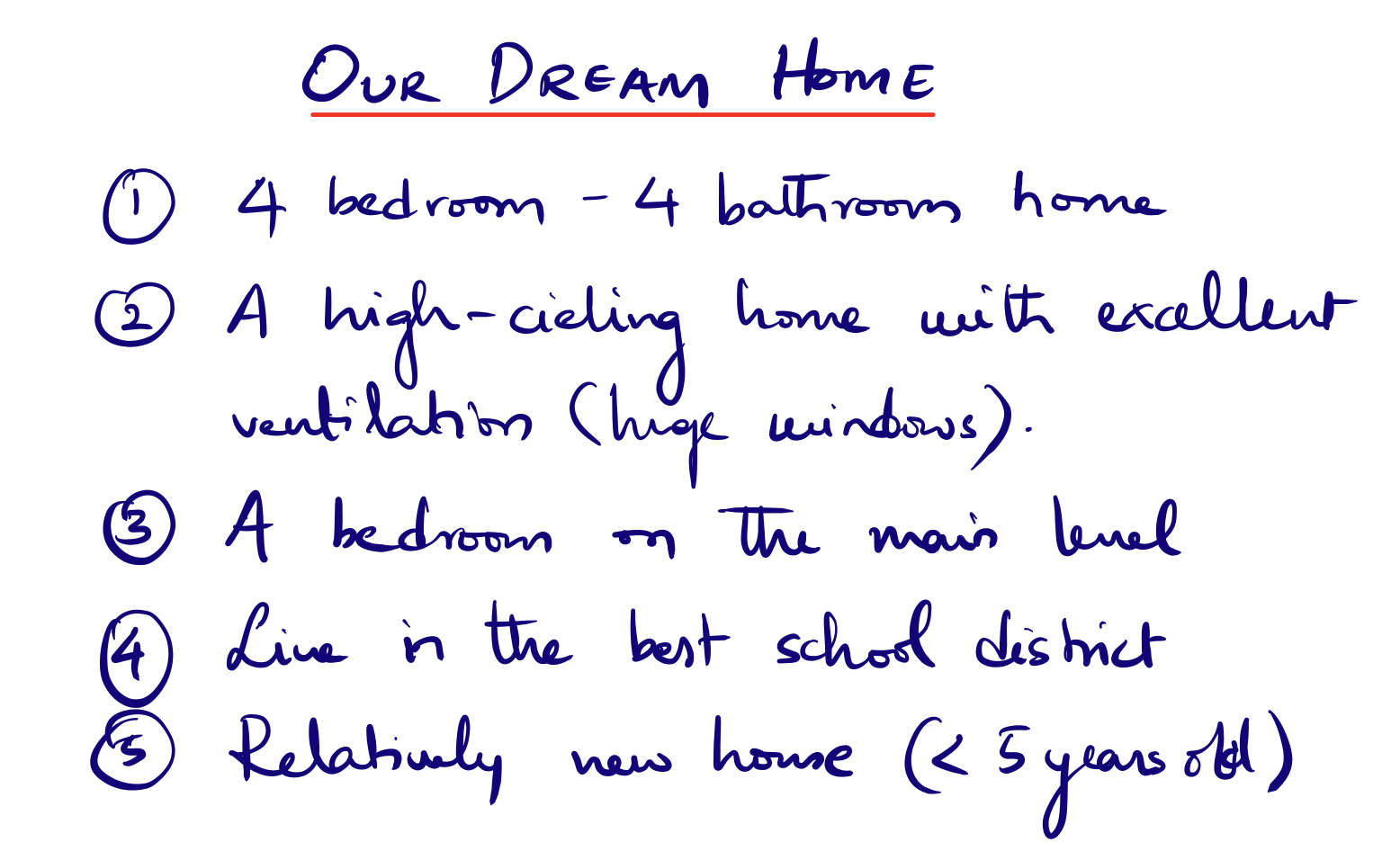

Prepare a checklist for your ideal home.

Decide on what you need in a home in terms of design features, number of rooms & bathrooms, floor plan, location, and age of the property.

Every once in a while, it is easy to get carried away when you see a visually appealing house. The checklist comes to your rescue to objectively cut through the temptations.

Realtors are not Your Knight in Shining Armor.

Realtors are like necessary evils. Nobody wants them, and everybody uses them. I often joke that most home buyers expect a Tom Cruise (Mission Impossible franchise) when looking for realtors and end up disappointed inevitably. My experience suggests that you should expect only one thing from the realtors: showing you as many homes as you want. For everything else, you have to do your research.

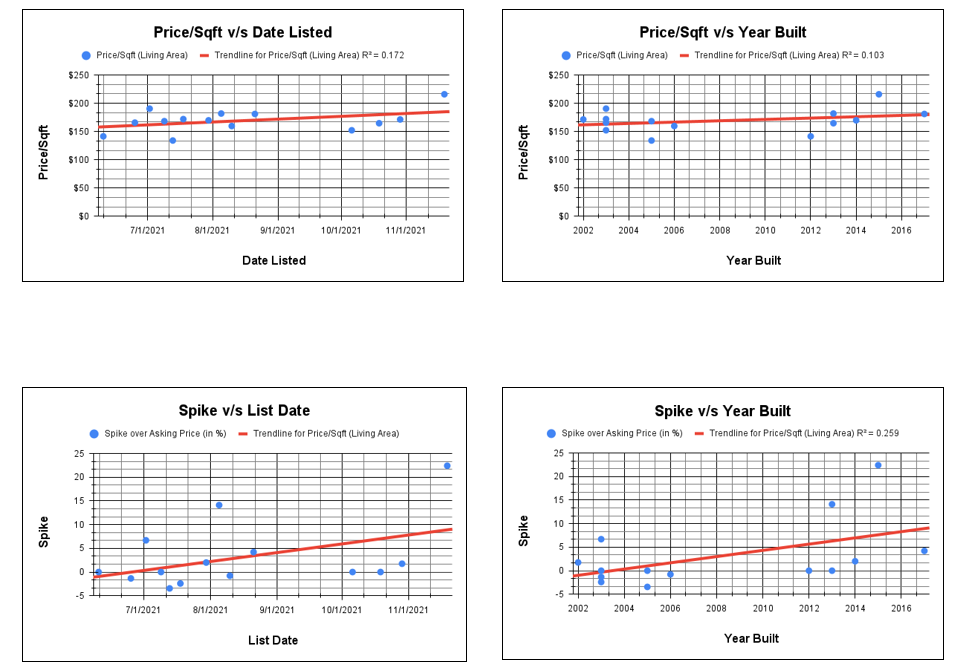

To arrive at the right price, you could analyze ten properties sold in the recent past in the area surrounding your desired home, as shown above. All the data is publicly available on most listing websites like Zillow, Redfin, etc.

To make an offer, you can look at different parameters as a function of the listing date and year of construction. It will help you make an educated guess of a winning offer price.

Finally, compare your numbers with realtor suggestions to ensure no blind spots. In my personal experience, realtors consistently overestimated home prices.

Appraisal/Inspection Contingencies are your Friends. Don't Waive Them

Appraisal contingency means that if your home doesn't appraise for the amount you've agreed to pay, you can walk away from the deal with your deposit.

A home inspection contingency mandates that the offer is contingent on the result of the home inspection. It ensures the buyer can collect enough information to make an informed purchase decision. Unless you know what you are doing, don't waive them.

While making an offer on our home, we included both appraisal and inspection contingency. Because we loved the house, I offered a slightly higher price than the market price. The bank appraised the house at the market price. We agreed to buy it midway between my original price and the appraisal price. I ended up saving a few thousand dollars.

Call the Lenders on the Same Day.

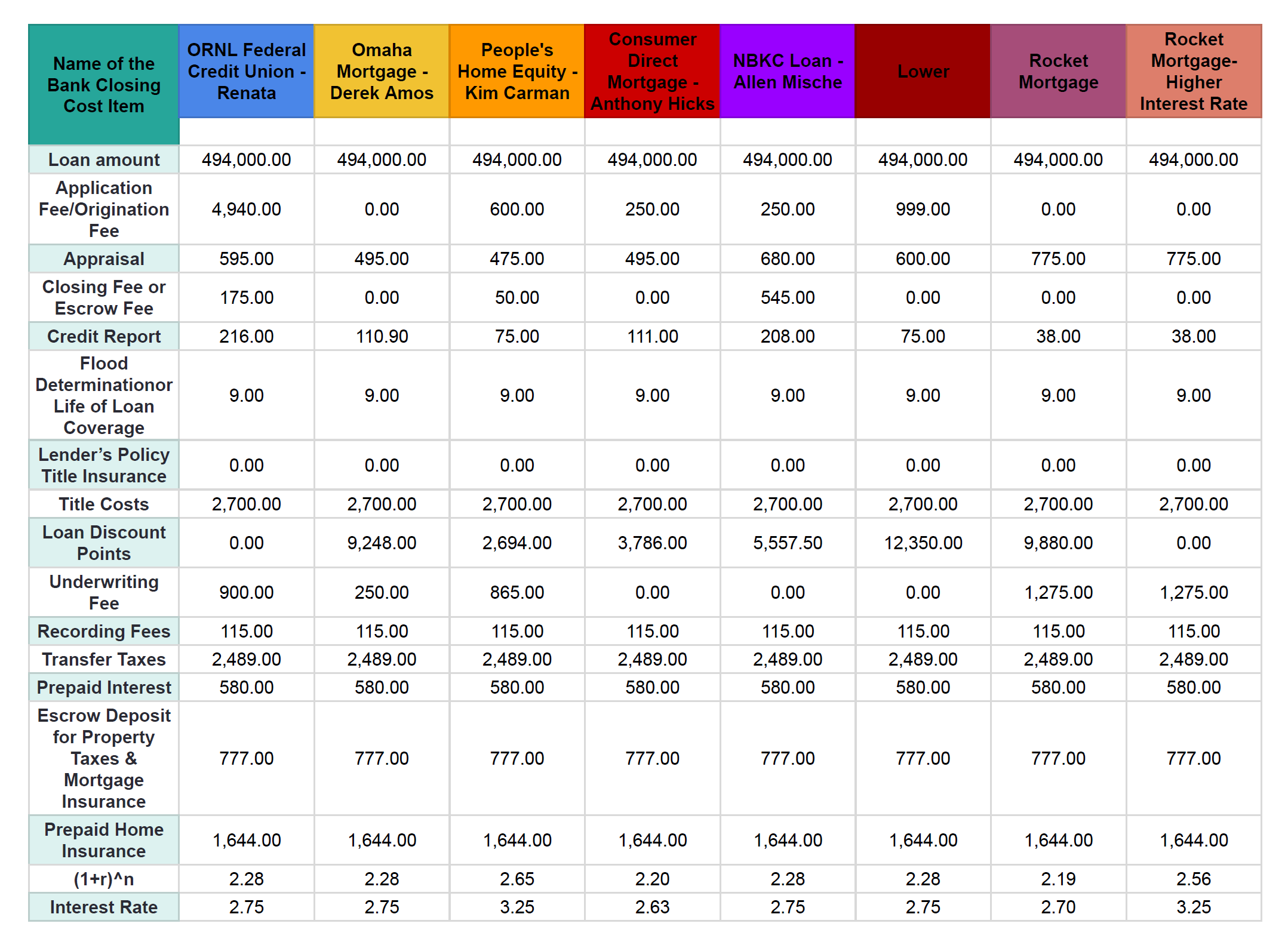

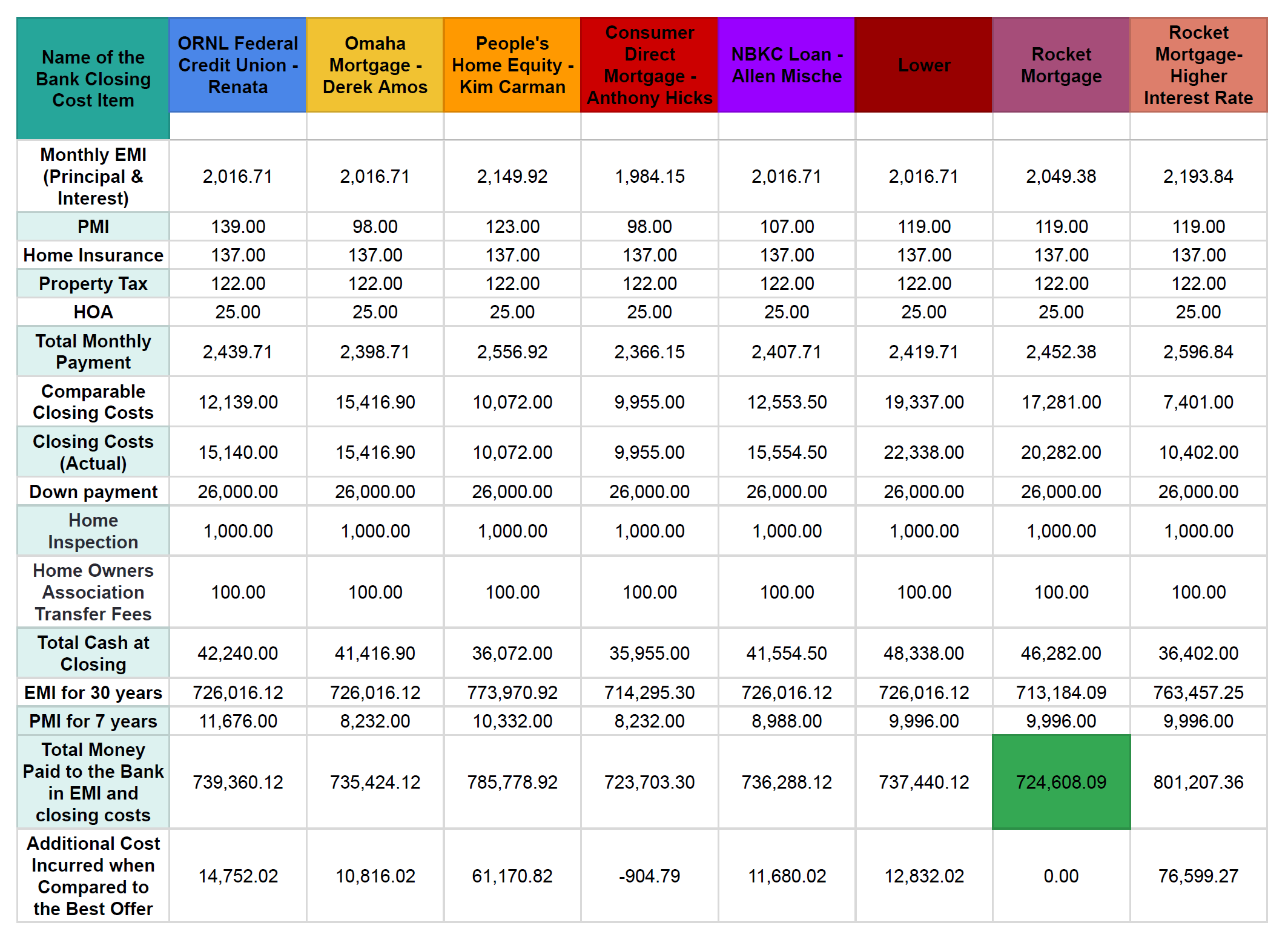

Once you have an accepted offer, call all the lenders on the same day. All lenders run a hard credit check before giving you an exact interest rate and closing costs. The credit check impacts your credit score negatively. If you space out your calls, every lender gets a different credit score (lower than the previous one) and offers a bad deal. It skews any analysis intended to compare other lenders. Hence, it becomes vital to call all of them on the same day. Experts suggest making all the calls within 45 days to prevent the impact of multiple credit checks impacting your score. However, it still leaves you open to changing interest rates and makes the comparison cumbersome.

Often, lenders overwhelm you with information, making it challenging to manage the numbers. It's always better to prepare an excel sheet, as shown below, and compare all numbers. Most lenders communicate entirely on the phone these days, and it becomes vital that you perform your due diligence with great attention to detail. Lenders are incentivized based on the number of loans they sell. So, whenever they expound on how they are better, ask them about specific fees and record it on an excel sheet to compare with other lenders.

Conclusion

Although I was initially against buying a home during the pandemic-induced hysteria, I changed my mind for two reasons.

- Home prices shot up because there was a genuine shortage on the supply side. COVID has wreaked havoc on supply chains worldwide, leading to slower construction of new homes.

- The Federal Reserve announced rate hikes to tackle inflation, meaning home loan interest rates would increase for a year or two to contain the price growth.

Delaying the purchase further would mean I would pay a higher price and interest rate for the same house down the line. As we were already passively looking for homes, we knew what we wanted and decided to jump in. Have we made a financially sensible decision? Only time will tell. I will revisit this decision once a year to see if it still makes sense.

If you like what you read, you should consider subscribing to my email newsletter. I send an email every week with a few thoughts, reflections, and curated links to interesting books, articles, and podcasts I've enjoyed.

Full Disclosure: Some of the links on this site are affiliate links, meaning, at no additional cost to you, I will earn a commission if you click through and make a purchase. But feel free not to use them.